Recently, shares of Amazon (AMZN) took a hit after the company's second-quarter earnings report. While top-line numbers and guidance looked very good, investors were spooked by the company's huge bottom-line miss and weak operating income guidance. In the end, the report basically continued the Amazon narrative, which is a company that spends heavily to keep its revenue growth flowing.

As the company continues to sell more from its third party marketplace, and the AWS business becomes a larger part of revenue, Amazon's gross margins have continued to rise. Unfortunately, this obscures the true state of business because operating expenses are rising at a much faster rate. In Q2, Amazon reported the following year-over-year increases in these income statement items:

Revenues: 24.84%

Gross margin dollars: 29.22%

Fulfillment expenses: 33.01%

Marketing expenses: 44.18%

Technology and content expenses: 43.02%

General and administrative expenses: 50.69%

Because the company's four main operating expense items increased at rates much faster than gross margin dollars, the company reported a 51% plus decline in operating income. Additionally, Amazon guided to Q3 operating income in a range of a $400 million loss to $300 million profit, compared to a $575 million profit in the year-ago period. Increased spending explains why the company missed EPS items by a mile and why Q3 bottom-line numbers are coming down substantially.

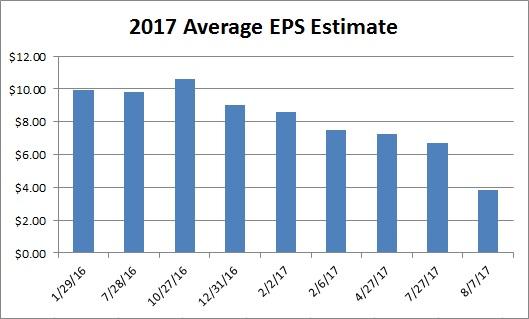

The real question to ask is, were these big bottom-line misses a surprise? For instance, we know Amazon has made numerous price cuts for AWS in recent quarters, which explains the 200-basis point decline sequentially in operating margins for the segment. Additionally, the reduction in the US to free shipping for orders over $25 means more smaller orders from consumers, which means a jump in the company's shipping expenses. Throw in increasing losses from the international business, and you have an ugly bottom line. Take a look at how street estimates have fallen:

At Monday's close, Amazon shares were down about $90, or about 8.4%, from their pre-earnings and all-time high. There seemed to be a lot of fear after the company's bottom-line disappointments, but if you follow the name, you really shouldn't be surprised. Amazon is spending heavily to grow, and top-line growth is still coming in at 20+ percent a year. If you are looking for profits, this is not the name to be in, but if you are looking for revenue growth, don't expect Amazon to go away anytime soon.

Disclosure:I/we have no positions in any stocks mentioned Read more .....

After a decade of experimenting with various options strategies, I have discovered a reliable approach to producing a steady 7% monthly return while protecting my investment. This strategy builds upon the principles of covered calls and calendar spreads, with a key twist. Traditional covered calls require significant capital and carry substantial downside risk if the stock price plummets. Calendar spreads, on the other hand, demand constant adjustments and have unlimited downside potential. The alternative strategy I've developed is a modified collar options strategy. It involves purchasing deep in-the-money call options with a longer expiration date and simultaneously selling at-the-money or slightly out-of-the-money call options with a shorter expiration date. Additionally, I buy out-of-the-money put options and sell way out-of-the-money put options with a longer expiration date. This approach has proven to be a reliable and consistent performer, offering a monthly return of over...

By Mike Welch To become a Hedge Fund Manager you will need to complete a level of education and also acquire specific professional certification. Because Hedge funds require background knowledge of how to work with sophisticated investment strategies and trade complex financial products, a strong proficiency in math and economics will be required. Hedge fund managers just starting out generally start as a junior trader and if successful can proceed to a career as a higher-level trader. To become a Hedge Fund Manager, planning should start as early as High school if you know that’s the career you aim toward. In order to become a Hedge Fund Manager, choosing the right college or university is the first step to success. Hedge Fund managers often invest through complex investment strategies and having the right college degree will allow them to run the fund effectively and profitably There are many universities that havebachelor’s programs in Business with a focus on economics or accoun...

By Joseph.L.Shaefer Seeking Alpha Summary Most science and technology funds are passively-managed and capitalization-weighted. All have done exceedingly well this year as the biggest of the big continue to gobble market share. At what point do some governments may decide these monsters are too big for their pantalones and restrain them or tax them into unprofitability? Here’s an interesting adjunct to ETF homogeneity that may fly under the political radar. We used to think of tech stocks as those engaged in science and technology that would likely change the way we live, defend our nation, build things, transport ourselves, secure resources, and so on. Somewhere along the way the “science” part got moved into the sectors with which they deal – aerospace firms into the Industrials sector, those pursuing interesting avenues in alternative energy into the Energy Sector, new hardware for medical diagnostics into the Health Sector, etc. What Big Tech is now is mostly produc...